UKGC Affordability Checks on NBA Betting Accounts: Thresholds, Triggers and Documents

The Question Nobody Wants to Get on Game 5 Night

The first time a UK book emailed me asking for proof of funds, it landed in my inbox at 03:14 BST on a Wednesday morning – about an hour after I’d placed a Game 5 in-play stake. The book had perfectly normal reasons to ask. I had perfectly normal documents to send. But the timing was awful, the panic was real, and I’d done nothing wrong. That’s the thing about UK affordability checks: they’re rarely catastrophic for compliant bettors, but they’re almost always inconvenient.

Since 28 February 2025, the UK Gambling Commission has run financial vulnerability checks on remote operators starting at a £150 net deposit threshold over a 30-day rolling window. The previous threshold was £500. The new number lands much lower in a typical Finals run, where a single intense series can take an account from «casual» to «checked» in under three games.

This article walks through what the £150 threshold actually triggers, the difference between light-touch vulnerability checks and full Financial Risk Assessments, what documents operators ask for, how the timing of a check during Finals week can disrupt a betting routine, and how to prepare so the check is a five-minute interruption rather than an account freeze.

The £150 Threshold Explained

The £150 figure isn’t a maximum stake or a single-deposit cap. It’s a net 30-day deposit threshold. Net means total deposits minus total withdrawals over the rolling 30-day window. A bettor who deposited £200 but withdrew £80 in the same period has £120 of net deposits and is below the threshold. A bettor who deposited £160 with no withdrawals has £160 and is above it.

The rolling-30-day mechanic matters because it changes how an NBA Finals run looks to the operator’s risk system. Imagine a UK bettor depositing £40 to back each of four Finals games across two weeks. Total deposits: £160. Withdrawals: zero, because the bets are still pending. Net 30-day: £160. The threshold has been crossed.

The UKGC estimates that around 3% of active accounts actually face an extended Financial Risk Assessment, and that light vulnerability checks affect roughly the same proportion. The numbers sound small in aggregate, but the population that crosses the £150 threshold is much larger than the population that ends up with a full FRA – most threshold crossings result in only a «light touch» check that’s resolved automatically by the operator’s system.

It’s worth noting how the threshold sits within UK gambling reform more broadly. From 21 May 2025, the UK imposed online slot stake limits of £5 per spin for players aged 25 and over and £2 per spin for 18 to 24 year olds. The slot limits and affordability thresholds are part of the same reform wave that came out of the 2023 White Paper. They share the same underlying logic – pre-empt harm at moderate levels of activity rather than wait for severe problem-gambling indicators.

Light-Touch Checks vs Full Financial Risk Assessments

The £150 net threshold triggers a light-touch check first, not a full FRA. Light-touch means the operator’s automated system runs publicly available data (credit-reference databases, basic identity verification, sometimes public records) against your account and the deposit pattern. The customer typically doesn’t see this check happening – it runs in the background and resolves without intervention in the majority of cases.

If the light-touch check flags something – unusual deposit pattern, mismatch between declared income and observed activity, account age inconsistencies – the operator escalates to a more involved check. This is where you might get an email asking for verification of identity, address, or source of funds. The escalated check is what most UK bettors mean when they say «I got hit with an affordability check.»

A full Financial Risk Assessment is the heaviest tier. It involves the customer submitting bank statements, payslips or other proof of income, and sometimes a brief questionnaire about gambling activity. FRAs affect around 3% of active accounts and are typically triggered by much larger deposit volumes than £150 – the threshold for an FRA isn’t published, but operator behaviour suggests it kicks in around £2,000-£5,000 monthly net deposits or in cases where light-touch checks have already flagged concerns.

The UKGC has been careful to emphasise that the light-touch checks should be «frictionless» for the customer in most cases. The reality is messier: customers report being asked for documents at unexpected moments, and operators have been criticised for treating low-risk customers as if they were already in trouble. Andrew Rhodes, the UK Gambling Commission’s Chief Executive, addressed the BGC AGM 2025 in February: «Recent data published shows that total gross gambling yield (GGY) is at its highest ever level at £15.6 billion. Participation in gambling has remained stable at 48%, just under half of the adult population in Great Britain.» His broader argument was that the regulated market was healthy enough to absorb sensible friction without losing customers – but the practical experience of the friction is what UK bettors actually deal with.

What Documents Operators Ask For

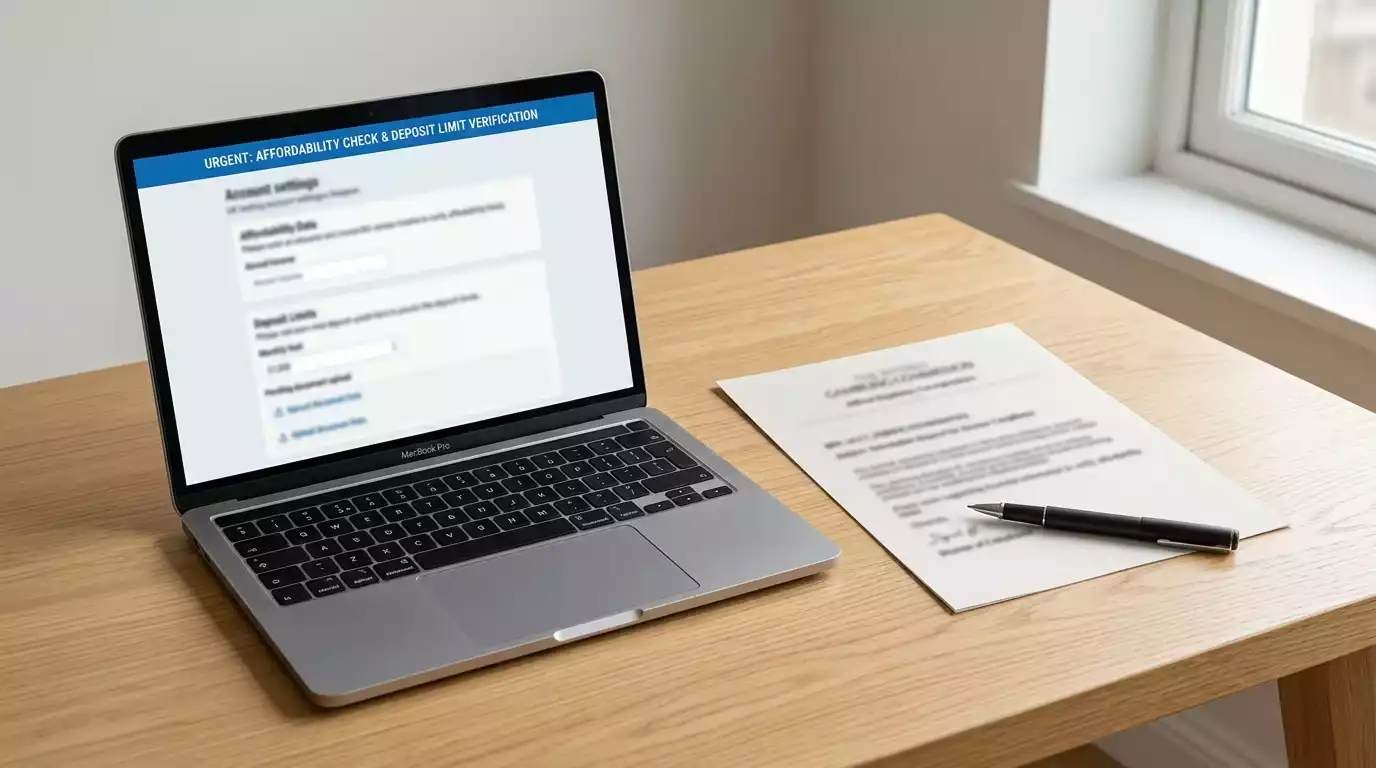

If you’re escalated past the light-touch check, the most common documents requested are: a recent bank statement (typically 3 months), a payslip or other proof of income, a utility bill or other proof of address dated within the last 3 months, and a copy of a government-issued ID if your account verification was thin to begin with. Some operators ask for a self-declaration of monthly disposable income alongside the documents.

The bank statement is the heavy lift. Operators look for two things: a stable income flow consistent with your stated occupation, and an absence of patterns that suggest gambling harm (multiple deposits to other operators, payday-loan inflows, late mortgage payments). They aren’t auditing your personal finances; they’re checking that your gambling activity is proportionate to your means.

Privacy concerns are legitimate. A UKGC survey in 2021 found that 77.6% of 12,000 respondents felt companies should not be required to assess customer affordability; 64.4% cited personal freedom and 61.4% cited privacy concerns. The regulatory response has been to limit data requests to what’s necessary and to require operators to handle documents under strict data-protection rules. Whether that satisfies the privacy concern depends on the bettor.

Practical tip: have a recent bank statement and payslip saved as PDFs somewhere accessible. If an operator asks, you can respond within minutes rather than scrambling. Operators typically give 24-72 hours to respond before account restrictions kick in, and a slow response during a Finals week can mean missing the Game 6 or Game 7 betting window entirely.

Timing During Finals Week

Affordability checks don’t pause for Finals games. The risk system runs continuously, and an account that crosses the £150 net threshold on Game 3 night might trigger a check that lands in the inbox on Game 4 morning. The check itself might take 24-48 hours to resolve. If you’re mid-series with pending stakes, the account restriction during that window can be brutal.

UK NBA fans grew their fan base 24% since 2022 according to UK government data, and as the audience grows, more first-time bettors arrive on UK books expecting US-style sportsbook UX. The UK reality is different – checks are part of the product, and the £150 threshold catches a wider swath of casual bettors than the previous £500 ever did.

The structural defence: don’t deposit in big lumps mid-series. A £200 deposit on Game 3 night is much more likely to trigger a check than spreading £200 across four deposits across the preceding two weeks. The threshold is cumulative, but the risk-flagging logic still notices spikes. Smoother deposit patterns get less attention than spike patterns of the same total amount.

Another defensive move: place some pre-Finals deposits earlier in the playoff window when there’s less urgency, so the Finals deposits sit on top of a lower-risk baseline rather than coming out of nowhere. The operator’s system sees pattern, not just total.

How to Prepare

The pre-Finals preparation routine I’d recommend has three parts. Part one – front-load documentation. Save a recent bank statement and payslip as accessible PDFs before the playoffs start. If an operator asks at 02:30 BST, you have 30 seconds, not 30 hours, of friction to deal with.

Part two – spread your deposits. Don’t dump £400 into an account on the morning of Game 1. Top up smaller amounts across the preceding weeks. The operator’s risk system reads smoother patterns as lower-risk, even when the total dollar amount is the same.

Part three – set deposit limits at the operator level before the playoffs start. Deposit limits aren’t a substitute for affordability checks (the operator still runs both), but they act as a behavioural baseline that supports the operator’s view of you as a controlled customer. A self-imposed £200 monthly deposit limit signals consistency, which feeds favourably into the risk profile.

UK Remote Gaming Duty rises from 21% to 40% from April 2026, with the new 25% Online Sports Betting Duty arriving in April 2027 to replace the current 15% General Betting Duty. As the tax pressure compresses operator margins, expect affordability check thresholds to receive more scrutiny – both from the regulator and from operators trying to keep good customers. The £150 threshold may move, may be enforced differently, or may be supplemented with new categories of «frictionless» check. Staying inside the spirit of the regulation – proportionate stakes, transparent funding, no signs of distress – is the durable strategy regardless of how the specifics evolve. The complementary tool – setting your own deposit limits before the regulator forces a check – is laid out step-by-step in setting up deposit limits on a UK NBA betting account.

What net deposit triggers an affordability check at UK NBA sportsbooks in 2026?

Since 28 February 2025, UK operators run financial vulnerability checks at a £150 net deposit threshold over a 30-day rolling window. The previous threshold was £500. Light-touch checks at the £150 level run automatically in the background; more involved checks and full Financial Risk Assessments kick in at higher levels of activity.

What share of UK NBA betting accounts actually face a full FRA?

The UK Gambling Commission estimates that around 3% of active accounts face extended Financial Risk Assessments, with light vulnerability checks affecting roughly the same proportion of accounts. Most threshold crossings at the £150 level resolve automatically without the customer being asked for documents.

Preparado por la redacción de «nba Final Bets».