NBA Finals Outright Odds in the UK: How Larry O’Brien Trophy Futures Move from October to June

Índice de contenidos

- Outright odds for a UK bettor: where the Larry O’Brien market actually lives

- What a futures price really pays you

- How UK books display the Larry O’Brien market

- The 2026 board, line by line

- Seven different champions and what that did to the price of a repeat

- Comparing UK books without falling into the aggregator trap

- Hedging a live futures ticket once the Finals are set

- The hidden cost in every outright market: overround

- Questions UK bettors keep asking me about outright odds

Outright odds for a UK bettor: where the Larry O’Brien market actually lives

The first outright ticket I ever placed on an NBA champion was a 16/1 on the Toronto Raptors in October 2018, written on the back of a Paddy Power receipt I kept in a desk drawer for eight months. By June it had paid the rent. That receipt is the entire reason I keep telling UK bettors that the Larry O’Brien futures market is not a single price — it is a slow argument between you and a bookmaker that runs from pre-season to the final buzzer of Game 7.

An outright bet — what UK books call a futures bet — is a single wager on which franchise will lift the Larry O’Brien Trophy at the end of the season. You pick the team in October, November or January, the book locks in the price, and the ticket either pays out in June or it doesn’t. There is no in-play, no cash-out forced on you, no per-game adjustment unless you choose one. The price you took is the price you live with, unless you actively trade out.

For a UK bettor that simplicity is the appeal and the trap. The appeal is that you only need to be right once across an entire season. The trap is that you are paid in fractional odds — 4/7, 7/2, 50/1 — at the time of writing, with OKC Thunder pinned at the short end and the field stretching out to four-figure prices on rebuilding rosters. Everything you read on US sites in pluses and minuses has to be translated, and the translation is where most edge gets lost. The rest of this guide is built on the fractional reading, because that is what your slip will show when you confirm the bet.

What a futures price really pays you

I learned the hard way that a futures bet is more like a bond than a stock. You hand the bookmaker a stake, you get a fixed coupon in return — the fractional price — and the only thing left is to wait. Eight months of waiting, in the case of an October ticket. People keep talking about futures as if they are aggressive plays. They are the opposite. They are the most boring product on the slip until the very last minute.

The mechanics are simple. You pick a team, the book quotes a price — say 11/2 on the Houston Rockets in early November — and your potential return is fixed the second the slip is confirmed. A £20 bet at 11/2 returns £110 in net profit plus your £20 stake, so £130 in the hand if the Rockets lift the trophy. Anything else and the slip is dead. There is no partial payout for losing in the Finals, no rebate for making the Conference Finals, no consolation if your team trades away its star in February. The price assumes the franchise wins every series it has to play.

The hold time is the part most newcomers underestimate. From the moment you place the bet to the moment it settles, the bookmaker is holding your stake for free. There is no interest, no float credited back, no recourse if the team fires its coach in December and the price drifts out to 25/1. You are locked in at the price you took. That is why the timing of an outright entry matters as much as the team. Pre-season prices are typically generous because the field of plausible champions is wide and the book has to price uncertainty into every line.

What you are actually buying is a small probability multiplied by a long delay. The 4/7 on OKC implies a 63.6% chance the Thunder win it all — at that price you are paid £17.50 for every £10 you risk if they do, but you have to hold the ticket for the entire post-season. The 50/1 on a fringe contender implies barely 2%, but the ticket sits in a drawer doing nothing until February, when an injury news cycle can either make the price look genius or send it to 200/1. Time, in futures, is the silent third party in every trade.

One detail UK bettors miss: cash-out on outrights is not a guarantee. Some books offer it, some do not, and the price they quote you to close early is almost always worse than the implied current market. If you want a real second leg on a futures bet, you trade it on the exchange, which I will get to a few sections down.

How UK books display the Larry O’Brien market

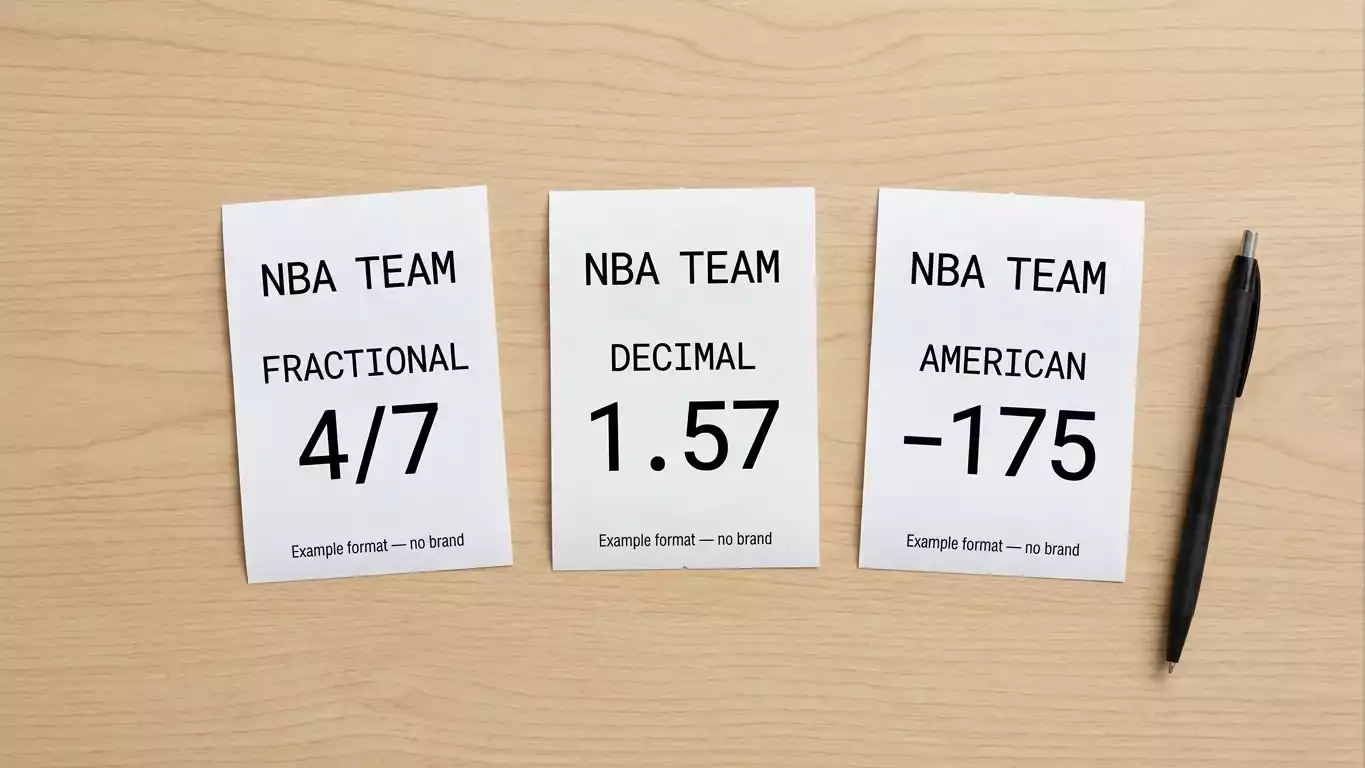

Walk into any UK-licensed sportsbook page in late October and you will see the Larry O’Brien outright market displayed in fractional first, because that is what the British punter expects and what the slip prints by default. Decimal is usually a toggle, sometimes buried in account settings, and American odds simply do not appear on a UKGC-regulated site. This is not a stylistic preference. It is a regulatory and cultural default that goes back to the high-street days, and it is still the only format on a printed betting slip in a Ladbrokes shop on Oxford Street.

Take the headline price of the season. At the time of writing OKC Thunder sit at around -175 to -180 on bet365’s US-style display, which converts to a fractional of 4/7 — roughly 1.57 in decimal. That is the format you will actually see on the slip. The Spurs are around +300 to +320 on the same US screens, which is 3/1 to 16/5 in fractional, or 4.00 to 4.20 in decimal. The Knicks are around +550, which is 11/2 in fractional or 6.50 in decimal. The point I want to drive home is that the number on your slip is fractional. The American number is for cross-checking against US analysts on Twitter at three in the morning.

Why does this matter for an outright bet specifically? Because the gap between formats opens up at the long end. A 50/1 outright on a third-tier contender reads cleanly in fractional and looks dramatic on the slip. The same number is 51.00 in decimal and +5000 in American. None of those is harder to compute, but only one is wired into your mental model of «how much does £10 make me if this hits.» Fractional answers that question instantly: £500 net profit plus your £10 stake. Decimal answers it by multiplication, which is fine for a calculator but slower on the floor.

The implied probability is what actually lets you compare prices across books. The formula for fractional is denominator over the sum of numerator and denominator. So 4/7 is 7 ÷ (4 + 7) = 63.6%. The 3/1 on the Spurs is 1 ÷ 4 = 25%. The 11/2 on the Knicks is 2 ÷ 13 = 15.4%. When I am comparing two UK books offering 4/7 and 8/13 on the same team, I do not compare the prices — I compare the implied probabilities. 8/13 is 13 ÷ 21 = 61.9%. That extra 1.7 percentage points of implied probability is the spread the second book is charging you for, and over a season of outright entries it compounds into real money.

One UK quirk worth flagging: William Hill, Paddy Power and Sky Bet have all historically priced the futures board with slightly different spreads at the long end. The favourites tend to converge — 4/7 here, 8/13 there — but the 33/1 at one shop is often the 28/1 at another, and that is where line shopping on outrights pays for itself.

The 2026 board, line by line

Most analysts I respect open this section with a table. I want to open it with a single number, because the rest of the board only makes sense relative to it. The number is 4/7. That is roughly the price the Oklahoma City Thunder are trading at on the Larry O’Brien Trophy, which on most US screens shows as -175 to -180, and it is the shortest a UK book has priced an October NBA favourite in years. The implied probability is 63.6%. The market is telling you that, by its assessment, the Thunder are more than a coin flip to come out of the entire post-season carrying the trophy. That is an extraordinary statement to make in October.

Below them, the San Antonio Spurs sit at roughly 3/1, which converts from a +300 to +320 US line. The board reads them as the only realistic Western Conference threat, on the back of a Wembanyama-led roster that has matured faster than the consensus expected. The Knicks come in at 11/2, the de facto Eastern Conference favourites, with the implied probability sitting around 15%. Below those three, the field stretches out fast. The Cavaliers, post-Game 7 survival against Detroit, are now priced at +2000, which is 20/1 fractional. They were +5000 — 50/1 — before that win. A single Game 7 result moved the implied probability from roughly 2% to 4.8%, which is a textbook example of how an outright price can swing on a single late-night result that most casual UK bettors slept through.

The structure of the board tells you what kind of market you are in. A short favourite plus a steep drop-off to the rest of the field is what bookmakers call a polarised board. The 4/7 on OKC, then a jump to 3/1 on the Spurs, then another jump to 11/2 on the Knicks, then the long tail starting at 12/1 and stretching out to 200/1 on rebuilding rosters — that shape is the shape of a market that has already made up its mind about the favourite. Compare that with the 2022-23 season, where the top of the board read at 5/1, 6/1, 8/1, 9/1 — a flat market with no consensus champion. The shape of the current board is closer to the 2017 Warriors board, when Golden State opened at 8/13 and never let the field catch up.

What the price is implicitly betting against is parity, and parity has been the defining feature of this league since 2019. A unique champion has appeared in every NBA Finals every year since 2019 — the longest such run in the league’s history. Seven different franchises in seven years. The 4/7 on OKC is, structurally, a bet that this seven-year streak ends here. The 33/1 on, say, the Houston Rockets or the Memphis Grizzlies, is the inverse bet — that the streak continues and a non-obvious team breaks through. For a UK bettor with a strong prior on parity, the long-tail value sits at 15/1 and longer. For a UK bettor with a strong prior on regression to talent, the 4/7 is fair, maybe even short.

What you do not get from any board, US or UK, is information about how the market got here. Every price on a futures screen is a closing price for the moment you see it. The Cavaliers at 20/1 today were 50/1 forty-eight hours ago. The Thunder at 4/7 today were 11/8 in July. Without that movement, the board is just a snapshot. With it, you can read where the smart money has already moved.

Opening lines versus where the board sits now

The cleanest record I keep of every season is a two-column spreadsheet: opening price in July, current price whenever I check. The gap between those two columns is the season’s narrative compressed into a single number per team. The OKC Thunder opened at around 11/8 in early July, which is 42% implied. They are 4/7 today, which is 63.6%. Twenty-one percentage points of probability have been priced into that team in four months, mostly on a perfect start to the regular season and a Western Conference that looks structurally weaker than scouts predicted.

For a UK bettor, the practical question is where to look for those opening prices, because UK books rarely advertise pre-season openers prominently. I scrape Pinnacle, which is not UK-licensed but publishes historical openers, and I cross-check against Oddschecker’s archive screenshots. The opener from a market-leader like Pinnacle is the closest thing to a clean «no-vig» baseline you will find. The fractional you eventually take at a UK book is then the closing price, and the difference between the two is your closing line value before the bet has even played out.

The shift in the wider UK market is part of why these openers matter more than they used to. The Gambling Commission’s chief executive Andrew Rhodes flagged the trend in early 2025, describing «a widening out of the sports offering» across UK operators, with basketball, cricket and US-based sports among the categories drawing fresh attention. NBA outright lines used to be a sleepy market with two updates per month. Now they move weekly, sometimes daily during big news cycles, and the gap between opener and current can compress or widen in a single news cycle.

Reading that gap is the first thing I do every morning during the season. If a team’s price has moved towards me — say I took 8/1 and the line is now 5/1 — I am in good shape regardless of what eventually happens, because the market has agreed with my read. If the price has moved away — I took 8/1 and the line is now 14/1 — I have to ask what the market is seeing that I missed.

Seven different champions and what that did to the price of a repeat

Ask me which single fact has done the most damage to repeat-champion prices in the last decade, and I will answer the same way every time: the seven-year streak. A unique champion has appeared in the NBA Finals every year since 2019, and that is the longest such run in the league’s history. Toronto in 2019. The Lakers in 2020. The Bucks in 2021. The Warriors in 2022. Denver in 2023. Boston in 2024. OKC in 2025. Seven different banners in seven years.

For a UK bettor the question is what this streak means for a price. It means that the implicit premium that bookmakers used to attach to a reigning champion — the «they know how to win in June» premium — has been almost entirely priced out. The Thunder, who won it all in 2025, are 4/7 today not because they are the defending champion but because their underlying numbers say they are by far the best team in the league. If the streak had been broken by, say, the 2017-19 Warriors three-peat continuing into 2020, the equivalent reigning-champion premium today would be visible at around 8/13 instead of 4/7. The gap between those two prices is roughly four percentage points of implied probability, and that is the parity discount baked into modern outright pricing.

The structural reasons are well understood inside the industry. The 2017 collective bargaining agreement and its successors created tax aprons that punish top-end roster construction. Player empowerment lets stars move between contenders rather than stay loyal to a single dynasty. The skill curve has flattened. Title windows are shorter. None of this is news to anyone who has watched the league for the last decade, but the implications for outright pricing are precise. Repeat-champion futures are systematically underpriced relative to historical base rates from the 1980s and 1990s — and that historical context, which I have written about in detail in how UK books price repeat-champion futures, is the single biggest gap between US-style analysis and what you will actually pay on a UK slip.

Here is the practical take. If a UK bettor is hunting value in October, the question to ask is not «is the reigning champion underpriced.» It is «is the reigning champion’s underlying talent overpriced relative to the team that is genuinely most likely to win.» Those are different questions. The 4/7 on OKC right now is not a repeat premium. It is a talent assessment. The fact that they happened to win last June is, in the eyes of the modern market, almost incidental.

Comparing UK books without falling into the aggregator trap

My ritual every Saturday morning during the season is one I have not deviated from in years. Open Oddschecker. Pull up the NBA Championship outright market. Scroll the column of UK books — bet365, William Hill, Sky Bet, Paddy Power, Ladbrokes, Betfred, Coral, BoyleSports — and screenshot the top six prices on every team in the top twelve. Then close Oddschecker, open each book directly in a separate tab, and verify. That verification step is the one most UK bettors skip, and it is the single most expensive habit you can develop.

Aggregators are useful because they collapse the price comparison problem into a single screen. They are unreliable because they pull prices on a refresh cycle, not in real time, and during a fast-moving market a Saturday-morning Oddschecker price can be five to ten minutes stale. On a flat board that is fine. On a steam-move morning — when, say, an injury report drops and the Knicks suddenly trade from 11/2 to 9/2 — the aggregator will still show the 11/2 for a few minutes after the book has already moved. Confirming a stale price is one of the easier ways to lose money you did not need to lose.

There is also a structural issue with aggregators that experienced bettors learn the hard way. The books that pay aggregators for placement have an incentive to show their best public-facing prices on Oddschecker and slightly worse prices on direct entry. Some operate the same prices everywhere. Some, demonstrably, do not. The only way to know which is which is to keep a private record of where the direct price agreed with the aggregator and where it did not.

For an outright bet specifically, the aggregator-vs-direct gap matters less than it does for a same-game parlay because the outright market moves slower and the prices are less volatile minute-to-minute. But the long-tail teams are where the discrepancies hide. Aggregators tend to show the median price across the field. The best UK price on a 33/1 team might actually be 40/1 if you check the long-tail boards at Sky Bet or BoyleSports directly. On a £10 ticket the difference between 33/1 and 40/1 is £70 of net profit, which is not a rounding error.

My standing recommendation to anyone serious enough about outrights to be reading this far is to use the aggregator as a starting point and the direct site as the source of truth. Treat Oddschecker as a list of books to check rather than a list of prices to take. The five minutes that adds to your routine pays for itself by the third outright bet of the season.

Hedging a live futures ticket once the Finals are set

The single best night of my betting life was watching the Raptors take Game 6 in Oakland in 2019, holding that 16/1 ticket I mentioned at the very top of this article. The single worst decision I made that night was not hedging. I should have laid roughly 25% of the ticket on Golden State at 6/4 the morning of Game 6, locking in a guaranteed profit no matter the result. I held the full position, won the whole thing, and have spent the years since explaining to clients why what I did was reckless rather than smart.

Hedging an outright in the UK is technically straightforward and emotionally hard. The mechanics: once both Finals teams are known, the Betfair Exchange will quote a «lay» price on each team — that is, a price at which you can bet against them rather than for them. If you hold a long-priced ticket on the team that made the Finals, you lay a fraction of that ticket on the opposing team. The fraction is calibrated so that no matter who wins the series, you take home a guaranteed amount. The maths is school-level arithmetic; the discipline is the hard part.

Here is a worked example. You hold £20 at 16/1 on a team that has made the Finals. If they win, the ticket returns £320 in net profit plus £20 stake, so £340. If you do nothing and they lose, you lose your £20. To hedge into a guaranteed £150 regardless of result, you lay enough of the opposite team on the exchange to cover that target. At a lay price of 5/4 on the opponent, the lay stake is calculated so that the winnings from the lay equal the £150 you want guaranteed if your team loses, and the cost of the lay subtracts cleanly from your £340 if your team wins. The numbers vary by the lay price and the target. The principle does not.

Tax sits in the background. Most personal betting in the UK is tax-free at the user level — the duties sit on the operators, not the punters. The new tax regime arriving from 2026 onward — Remote Gaming Duty rising from 21% to 40% in April 2026, and a new 25% Online Sports Betting Duty replacing the older 15% General Betting Duty from April 2027 — will compress the prices the books offer over the coming seasons, which makes the discipline of hedging at favourable exchange prices more valuable, not less.

The reason most UK bettors do not hedge is psychological. Locking in £150 of guaranteed profit feels like settling for less than the full £340. It also feels like admitting you might be wrong. The professional view is the opposite. Hedging is what converts a speculative bet into a realised return, and a realised return is the only kind of return that pays the rent.

The hidden cost in every outright market: overround

Here is a question I ask every new client in our first conversation. If the implied probabilities of every team on the championship board added up cleanly, what number would they total? Most answer 100%. The actual answer, on a typical UK outright board, is somewhere between 110% and 120%. That extra 10–20% is the bookmaker’s overround, also called the vig or the juice, and it is the structural cost of every outright bet you place.

The way to see it on your own screen takes ninety seconds. Pull up the full board on any UK book, convert every fractional price to its implied probability, and add them all up. For a 30-team market like the NBA outright, you will land somewhere around 115%, with the favourites contributing the largest absolute share and the long tail contributing a smaller individual share but a meaningful cumulative chunk. The «extra» 15% is the margin the book builds in to guarantee a long-term profit regardless of which team eventually wins.

For an outright bet specifically, the overround is more punishing than it looks because of the hold time. On a 90-minute football match the overround compresses to single digits because the market clears quickly and prices are tight. On an eight-month NBA outright, the book is holding your stake for the full duration with no risk of you withdrawing, no interest paid, and the comfort of knowing the cumulative implied probability is well above 100%. That is why long-term EV on outright bets is harder to extract than on game-by-game markets. The structural cost is higher, and the only way to beat it is to take prices that are demonstrably better than the no-vig fair price.

The practical implication is that line shopping is not optional. If bet365’s overround on the championship board is 118% and Pinnacle’s no-vig fair price would imply a 113% market, then taking the bet365 price on the favourite is structurally worse than waiting for a better quote elsewhere. Over a season of outright bets, the difference between consistently taking the best UK price and consistently taking the median UK price is the difference between a flat year and a positive year. The overround is silent. It does not show up on your slip. It only shows up in the closing balance of your account.

Questions UK bettors keep asking me about outright odds

When do UK sportsbooks open the NBA championship futures for a new season?

Most major UK books — bet365, William Hill, Paddy Power, Sky Bet — post initial Larry O’Brien Trophy prices in early July, within days of the NBA Finals concluding the previous June. The boards are thin at that stage, often only covering the top fifteen contenders, and the prices are deliberately conservative. Full thirty-team boards typically arrive in late September as pre-season tips off, and the lines tighten through October once the regular season begins and the books have ten games of fresh data to price against.

Can I cash out an NBA outright bet before the Finals are decided?

Cash-out availability on outright tickets varies by operator and is never a guarantee. Some UK books offer it on long-running futures, some do not, and the books that do quote a cash-out price that is typically worse than the implied current market by a meaningful margin. For a real hedge on a futures position, the Betfair Exchange is the cleaner instrument because you can lay the opposing position at a transparent market price rather than accept whatever cash-out figure the book chooses to display.

Why are fractional odds on the NBA title usually shorter than the decimal equivalent in the US would suggest?

They aren’t actually shorter once you do the maths — they look shorter to a UK eye because fractional compresses the visual range. The 4/7 on OKC reads as a tight price, but 4/7 converts to 1.57 in decimal and -175 in American, which is the same price expressed three ways. The illusion comes from the fact that fractional makes the favourite-versus-field gap look narrower than decimal does on the same screen. The underlying implied probability is identical across all three formats.

Creado por la redacción de «nba Final Bets».